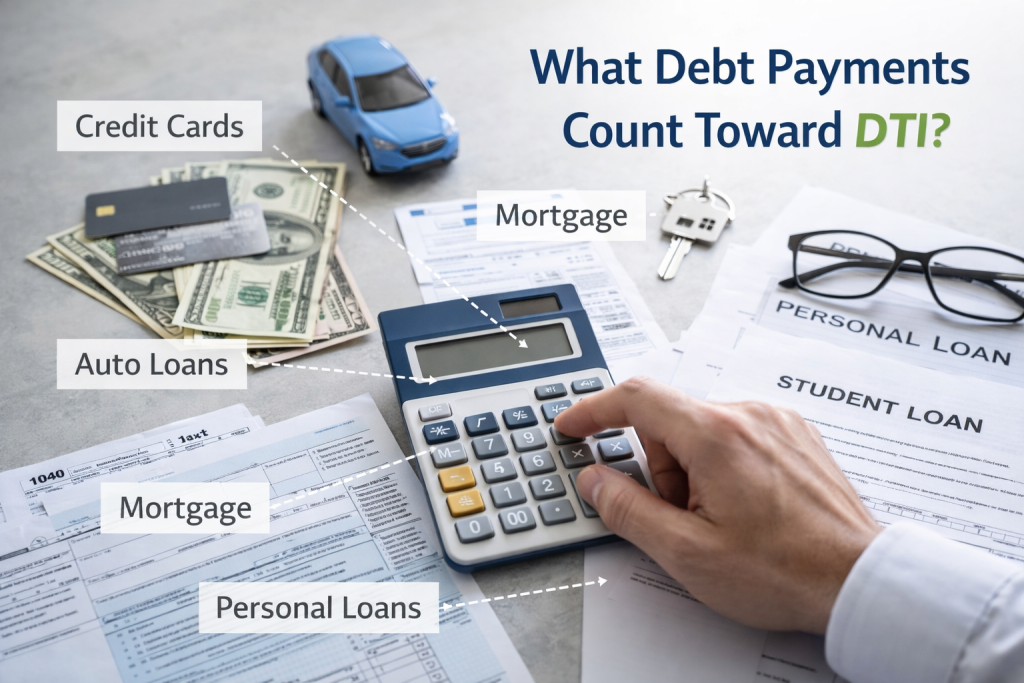

![]() The DTI ratio is calculated by dividing your total monthly debt payments by your gross monthly income. Lenders use this percentage to quickly assess your capacity to take on new debt.

The DTI ratio is calculated by dividing your total monthly debt payments by your gross monthly income. Lenders use this percentage to quickly assess your capacity to take on new debt.

The debt-to-income ratio (DTI) is a fundamental financial metric used by lenders to assess a borrower’s capacity to repay debt. At its core, it represents the proportion of a borrower’s gross monthly income that is allocated to meeting their total monthly debt payments. This ratio provides a snapshot of an individual’s or business’s ongoing financial obligations relative to their earnings. For instance, if an individual earns a gross monthly income of $6,000 and has total monthly debt payments amounting to $2,000, their DTI would be approximately 33% ($2,000 / $6,000 x 100). A lower DTI generally signifies a healthier financial situation, indicating that a larger portion of income remains available after debt servicing, thus presenting a lower risk profile to potential lenders.

Debt-to-income ratio is one of the most important factors lenders evaluate when approving startup loans. Learn how DTI works, what lenders prefer, and how to improve your financial profile before applying for business funding.

Open collections can impact your startup loan approval, but they don’t automatically disqualify you. Learn how lenders evaluate credit history, what matters most, and how to strengthen your application for business financing.

How long after credit damage can you qualify for a startup loan? While late payments, collections, or bankruptcy can impact approval, lenders focus on recovery trends, financial stability, and recent payment behavior. Learn how long different types of credit damage affect your eligibility and what steps you can take to improve your chances of securing startup funding faster.