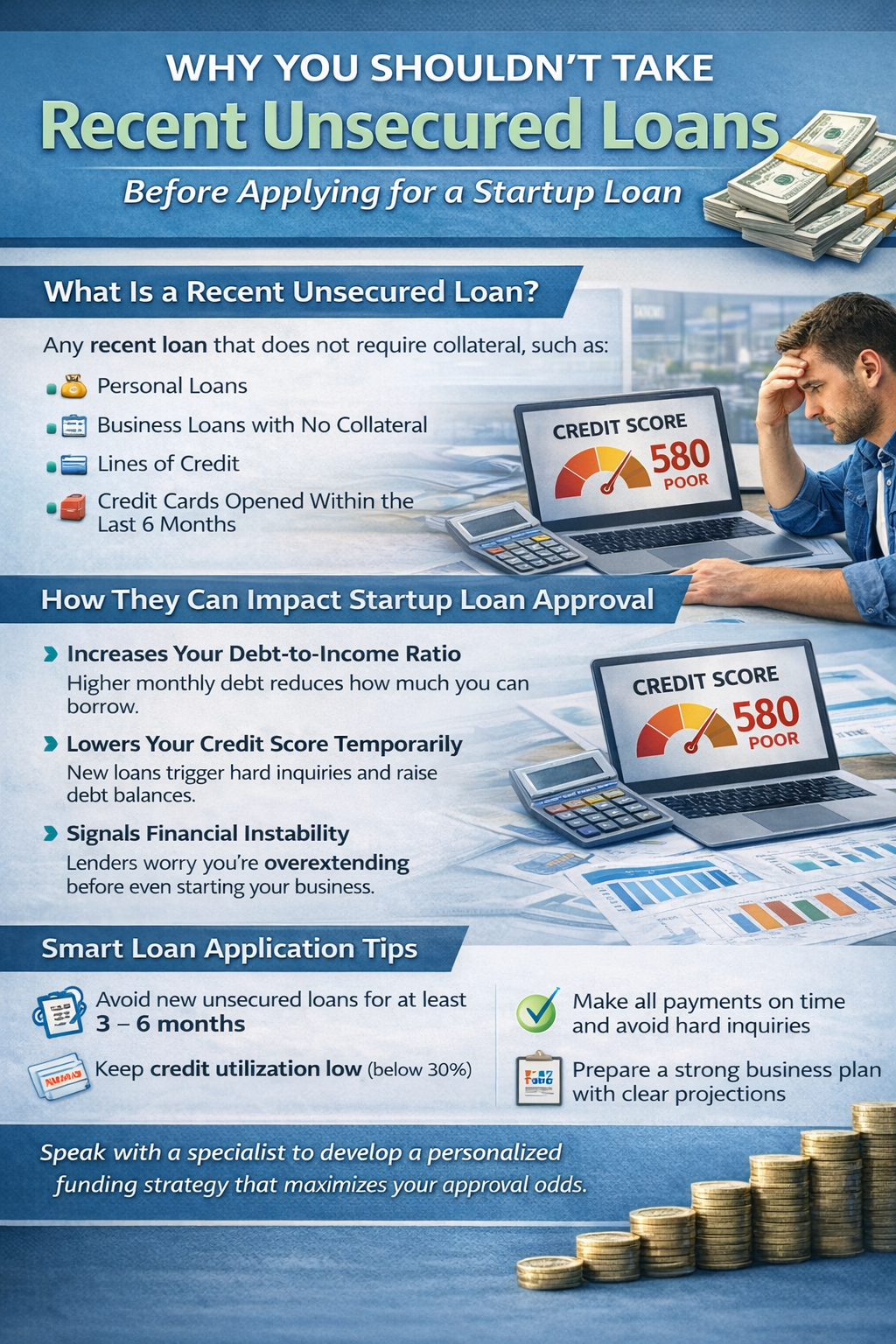

![]() Common types of recent unsecured loans that lenders scrutinize during a startup loan application.

Common types of recent unsecured loans that lenders scrutinize during a startup loan application.

Before discussing the impact, it is important to define what a “recent unsecured loan” means in the context of applying for business financing, especially small business loans and SBA loans.

An unsecured loan is any borrowing that does not require collateral, such as real estate or business assets. These loans are often chosen because they are faster and easier to obtain than secured loans.

Common examples include personal loans used for startup costs, high-limit credit cards for working capital, short-term loans, and unsecured lines of credit.

“Recent” usually refers to loans taken within the last 6 to 12 months before applying for a startup loan. This is the timeframe lenders review most closely when evaluating financial behavior and risk.

These loans are attractive because they require less documentation than traditional bank financing. However, they often come with higher interest rates and shorter repayment terms. That can reduce your future borrowing power.

According to Purbeck Personal Guarantee Insurance, 46% of personal guarantee insurance applications in Q1 2024 were for unsecured loans. This highlights the level of personal risk often involved.

Open collections can impact your startup loan approval, but they don’t automatically disqualify you. Learn how lenders evaluate credit history, what matters most, and how to strengthen your application for business financing.

How long after credit damage can you qualify for a startup loan? While late payments, collections, or bankruptcy can impact approval, lenders focus on recovery trends, financial stability, and recent payment behavior. Learn how long different types of credit damage affect your eligibility and what steps you can take to improve your chances of securing startup funding faster.

Taking recent unsecured loans before applying for a startup loan may reduce approval odds, increase interest rates, and lower funding amounts. Learn how credit score impact, debt-to-income ratio, and timing affect your ability to secure business financing.